The short answer: Most Ontario homeowners can tap between 65% and 85% of their home value, depending on your mortgage balance, lender type, and property location.

But the long answer? That’s where things get interesting — and where most homeowners get confused.

This guide breaks it all down in simple terms, using real private-lender math, not bank brochure talk.

🔍 1. What Determines How Much You Can Borrow?

Home equity lending in Ontario depends on four key factors:

1. Your Home Value

Higher value = more room to borrow.

Private lenders (like Lendworth) confirm value using comparable sales, market data, and sometimes an appraisal.

2. Your Current Mortgage Balance

The lender subtracts what you owe from what your home is worth.

This is your usable equity.

3. Your Loan-to-Value (LTV) Limit

Banks lend up to 65–80% LTV.

Private lenders lend up to 80–85% LTV depending on location and risk.

4. Your Property Type & Location

Some areas (Toronto, Vaughan, Oakville, Richmond Hill) qualify for higher LTV.

Rural + remote areas usually get lower limits.

🧮 2. The Actual Formula (Simple Math)

Here’s exactly how lenders calculate it:

Maximum Borrowing = Home Value × LTV − Existing Mortgage

Let’s say your home is worth: $1,000,000

Private lender max LTV: 80%

You owe: $450,000

$1,000,000 × 80% = $800,000

$800,000 − $450,000 = $350,000 available

✔️ You can borrow about $350,000 tax-free from your equity.

🏡 3. Average Borrow Amounts in Ontario (2025 Data)

From real private-lender files (including Lendworth-style deals):

| Home Value | Typical Available Equity |

|---|---|

| $600,000 home | $100K–$170K |

| $800,000 home | $150K–$250K |

| $1,000,000 home | $200K–$350K |

| $1,500,000 home | $300K–$500K |

| $2,000,000 home | $400K–$700K |

These vary by credit, location & existing mortgages — but this is the real Ontario range.

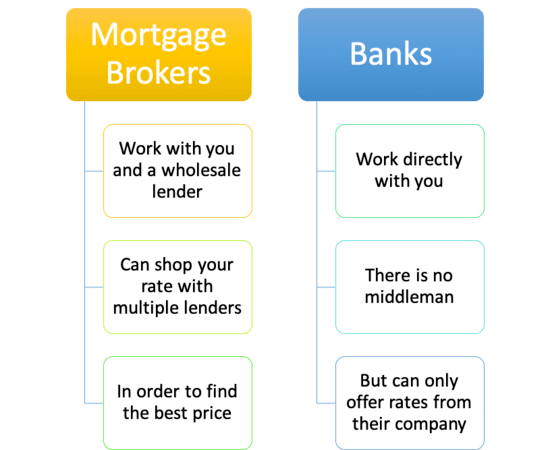

🏦 4. Bank vs. Private Lender Borrowing Amounts

Banks (BMO, RBC, TD)

Max LTV: 65–80%

Slow approvals

Heavy income verification

Strict credit rules

Great rates — if you qualify

Private Lenders (Like Lendworth)

Max LTV: 75–80% depending on city

Same-day approvals

Credit doesn’t matter

Equity-focused

Flexible terms

If you're self-employed, behind on payments, or declined by the bank, private lenders unlock much more borrowing power.

💰 5. What Can Homeowners Use the Money For?

Ontario homeowners tap equity for:

Debt consolidation

High-interest loan payoff

Second mortgages

Home renovations

Investment opportunities

Business cashflow

Emergency expenses

Bridge financing

Stopping Power of Sale

Equity is flexible — you can use it for almost anything.

⚡ 6. Quick “How Much Can I Borrow?” Cheat Sheet

| Situation | Likely Borrow Limit |

|---|---|

| Good credit + bank loan | Up to 80% LTV |

| Bruised credit, bank decline | 75–80% LTV |

| Self-employed, stated income | 75–85% LTV |

| In arrears or behind on taxes | 70–80% LTV |

| Rural / small towns | 60–75% LTV |

🏘️ 7. Property Location Matters

Ontario cities with highest LTV approvals:

Vaughan

Toronto

Richmond Hill

Markham

Mississauga

Oakville

Barrie

Innisfil

Newmarket

Aurora

Small towns & rural areas are typically 5–10% lower.

📈 8. Want the EXACT Number for Your Property?

Generic calculators are useless — they don’t use lender data or real comps.

Lendworth built EquityCheck™ to give a real lender-grade estimate of your home value & usable equity.

👉 Get your free Lendworth EquityCheck™ report now

https://www.lendworth.ca/equity-check

It includes:

✔️ Real comparable sales

✔️ Estimated LTV eligibility

✔️ Maximum borrowing amount

✔️ Lending options

✔️ Personalized recommendations

✔️ Same-day follow-up